On July 31st, 2019, Senator Cortez Masto of Nevada introduced a bill before the 116th Congress of the United States called the “Small Business Administration Franchise Loan Transparency Act of 2019.”

The bill’s stated purpose is “to establish minimum standards of disclosure by franchises whose franchisees use loans guaranteed by the Small Business Administration.”

This bill is critical to the health of the United States economy because franchising is a huge part of U.S. business. Its endemic fraud is with us. Right now, franchiSEES are scared and they’re still being silent. But things aren’t going to stay that way for long. The cat is almost out of the bag.

.

.

Taxpayers need to understand that they back all loans made by the Small Business Administration.

A franchiSOR is the corporate owner of the local franchised businesses you know and love: Subway, 7-11, Little Caesars, Kumon, Meinke, Dunkin’ Donuts and more.

FranchiSORS use the money of independent franchiSEES to spread their businesses across the United States and world, competing with your local independent small business owners who do not have the mass brand name recognition enjoyed by the FranchiSORS.

A franchiSEE is an individual: a United States citizen, a veteran, or a legal hard-working immigrant who wants to use corporate franchiSOR brand recognition to start a business.

But the franchiSORS aren’t playing fair.

Many deceptively sell franchise locations to trusting and vulnerable individuals who want own their own businesses and align themselves with larger corporate buying power, advertising and branding. *[See note at bottom of post.]

Through using the investment of the individual franchiSEES, the corporate franchiSORS are often able to force the small local independent mom-and-pop shops out of business because without access to corporate brand recognition and advertising, your local friends who own a pizza place often just can’t compete. Franchised businesses win consumer dollars.

In order to get the business advantages over the mom-and-pop shops, local franchiSEES are asked to sign dangerous franchise agreements with the corporate franchiSORS, initialing ALL CAPS statements that revoke their basic rights and even signing personal guarantees that could allow the franchiSOR to take away their home should their franchise location “fail.”

Many new franchiSEES also choose this arrangement because they believe that they are going into business “for themselves but not by themselves.” The choose to sign a franchise agreement because they trust the franchiSOR and want the support and business education the franchiSOR promises them.

The franchiSOR uses the investment of the franchiSEE to expand business.

When the Small Business Administration offers taxpayer-backed franchise loans, the loans are made to the smaller, more vulneraable franchiSEE rather than to the more powerful corporate franchiSOR.

In a nutshell, the loan goes to the franchiSEE but the investment goes to the franchiSOR.

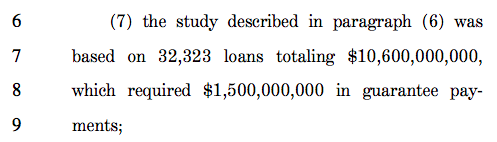

In September of 2013, the Government Accountability Office published a study based on $10,600,000,000 in SBA loans made to franchiSEES requiring $1,500,000,000 in guarantee payments… payments guaranteed by the more vulnerable franchiSEES’ homes and life savings.

When a franchiSEE-owned franchise location “fails,” the SBA can take its guarantee payments and the franchiSOR can sue the franchiSEE for anything that’s left because the franchiSEE signed a dangerous contract with the franchiSOR. The litigation is highly agressive.

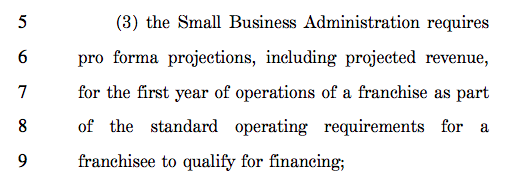

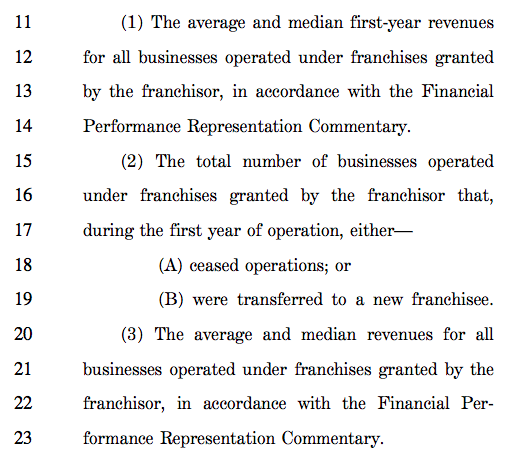

Right now, corporate franchiSORS are required to offer the Small Business Administration first-year revenue projections in order for the franchiSEE to qualify for the loan.

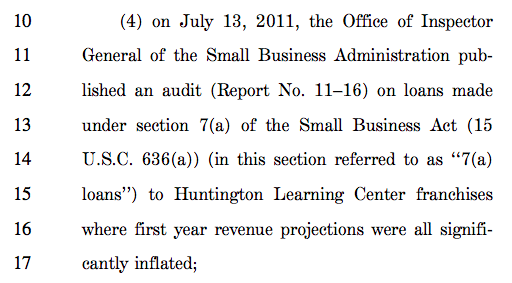

But unfortunately, the Small Business Administration has audited the franchiSORS’ projections and found they were “all significantly inflated!”

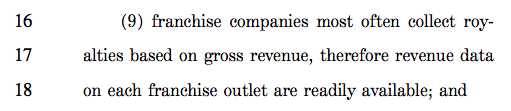

The corporate franchiSORS know the real amount of money the franchiSEES in their system are making.

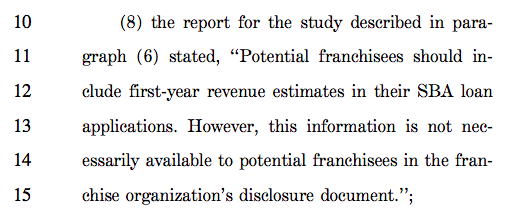

But in many cases, they’re not transparently disclosing those numbers to the franchiSEES themselves! The franchiSEES are asked to sign the dangerous contracts without knowing how much other franchiSEES are making with the business!

In order to affiliate with corporate franchiSORS, the francihSEES are basically asked to “trust” in the brand name of the franchiSOR because the franchiSOR isn’t required to disclose past revenue from other outlets.

This bill seeks to change that. This bill seeks to force franchiSORS to disclose past revenue numbers to franchiSEES whenever SBA loans are used.

Franchisors who want to qualify for SBA lending would have to make additional disclosures in the Franchise Disclosure Document the franchiSEES receive before they sign the dangerous contracts with personal guarantees or take out the SBA-backed loans (Act, page 5).

If the bill passes, franchiSORS will have to disclose:

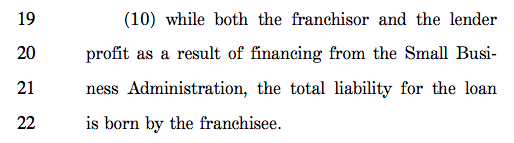

Taxpayer-backed SBA loans are made through banks. The banks make the loans and then sell them. The banks benefit.

(Is this bringing another financial crisis to mind?)

The corporate franchiSORS benefit because they use the money lent to the franchiSEE to expand their business reach and promote their brand.

The franchiSEES sign dangerous contracts, take all the risk, and often lose everything. Many of the franchiSORS businesses that qualify for SBA loans were never viable in the first place (remember those inflated pro forma promections given to the SBA!). FranchiSORS keep selling the dead-end franchises because they can. They make money off of franchise sales and nobody’s stopping them.

And in the end, the taxpayer loses, too, because the government is backing the loans.

But, even so, the International Franchise Association is lobbying against the bill.

* One commenter on LinkedIn offered this feedback about my article:

“This article is deceptive in it’s own right. It makes it sound as though all franchisors are deceptive and franchise candidates are complete victims with no responsibility for their own due diligence. As an example, it indicates one franchisor misclaimed revenue but the article made it sound as if all franchisors were guilty of this practice. There are numerous instances where the article wrongly accuses franchisors as being unscrupulous or is outright misleading. This is absolutely not an accurate portrayal of the industry. Franchisors who deceive their franchise candidates are despicable but so are articles that misrepresent an industry.”

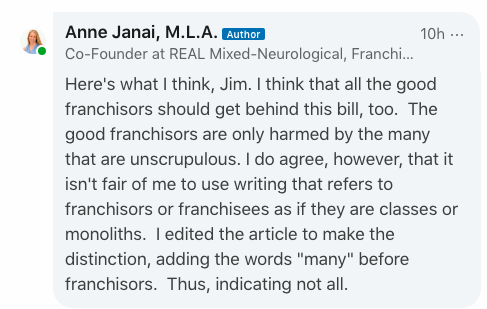

My response was:

Although I do believe that it is generally ill-advisable to refer to groups of people as classes or monoliths, I have no evidence that any franchiSOR refrains from using personal guarantees and ALL CAPS clauses in their contracts requiring franchiSEES to revoke their basic rights.

In addition, another commenter pointed out that:

“Franchisors have protected themselves from lawsuits by incorporating an “integration” clause into their contract. It’s pretty much one sentence (out of a 50 page doc) that states the franchisee did not rely on any information outside of the contract to make the purchase decision.”

Until I get information that there are some franchiSORS that are examples of not using these unscrupulous strategies to ensure a position of extreme power over their franchiSEES once the contract is signed, I will assume that franchiSORS are, in fact, a monolith in this situation.

I look forward to someone offering me evidence to the contrary. I will gladly accept it and write about it if it is available.

What I want is for the good franchiSORS to come forward and support the franchiSEES so that the industry can be fixed for everyone’s benefit.